Opinion

Revenue optimisation is increasingly important to the sustainability of universities as they move deeper into a constrained environment for international student growth.

As commencements become structurally constrained, international revenue will increasingly be determined by how effectively universities manage yield, mix and retention, rather than volume alone.

We recognise that both universities and international students also play a much broader and essential role, including economic contribution, soft‑power benefits and contributions to cultural diversity; however, this article focuses specifically on the income and financial implications of recent policy changes.

While universities have maintained growth in international enrolments, recent New Overseas Student Commencement (NOSC) ‘soft caps’ will now hit growth harder as uncapped, post-covid cohorts from 2021-23 complete their studies and capped cohorts replace them entirely.

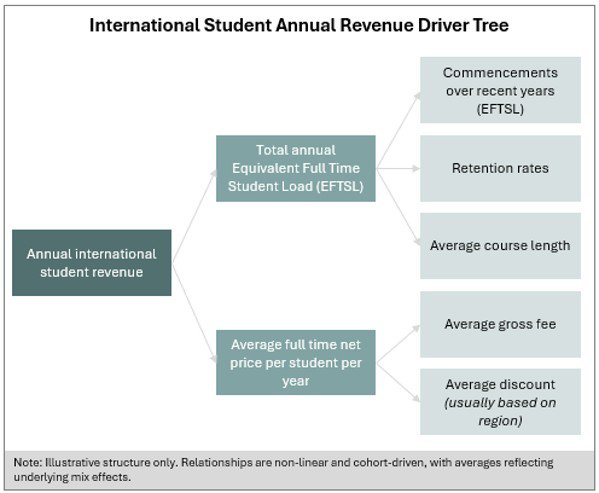

Universities need to fine‑tune their international student strategy by optimising the balance between volume and yield. Universities have 5 levers to pull:

- Commencements: Increasing the number of new students through successful bids for higher NOSC allocations and stronger demand generation, conversion and channel performance.

- Student retention: Improving students’ propensity to remain enrolled by reducing attrition and supporting progression throughout the course lifecycle.

- Course length: Shaping course mix toward longer‑duration programs (e.g. double degrees) which increases total enrolments at any point in time.

- Average gross fee: Managing pricing through course mix and fee settings, balancing headline prices with market willingness to pay and competitive positioning.

- Discounting: Actively managing scholarships and incentives to optimise net price per student without materially undermining demand, mix or retention.

Pulling these levers involves trade-offs for universities, underscoring the need for fine tuning to optimise revenue.

The policy changes will require universities to tightly optimise their use of those levers. While there are limitations and trade-offs within, universities can respond to the policy by increasing prices, reducing discounts and ‘bidding’ for higher NOSC caps by increasing purpose-built student accommodation and adjusting the student mix.

We have provided strategic analysis of 3 categories of universities, Group of Eight universities, Other metropolitan universities, and regional universities.

Group of Eight Universities: Typically, these universities have benefited from strong enrolments from high willingness‑to‑pay, high‑retention source markets, with students receiving lower discounts and enrolling in higher‑yield courses. They have received some of the lowest NOSC cap increases, reflecting constraints on expanding student accommodation in expensive metropolitan markets and limited appetite to shift away from high‑value source markets.

As a result, these institutions are likely to prioritise yield over volume, relying on pricing and discount discipline to lift revenue, supported by strong brand positions, premium course offerings and lower price sensitivity in core markets.

Other Metropolitan Universities: The policy changes have created opportunities for these universities to either pursue volume-driven revenue growth, where there are opportunities to increase caps and attract excess demand, or pursue yield-driven growth where ability to increase caps is limited. We are seeing some metropolitan universities use strengths in QS rankings and employment outcomes in specific broad fields of education to lift net prices in those courses. We have seen this support per student yield increases of 5-15% with minimal impacts on commencements. Those with higher allocations can pursue volume growth by capturing unmet demand, while constrained institutions need to focus on yield, course mix and conversion.

Regional Universities: Regional universities appear to be the main policy beneficiaries in allocation terms, receiving larger proportional increases as government seeks to distribute international education growth more evenly. The constraint for regional universities may be less about allocation and more about demand generation, channel strength, conversion and student experience. Revenue upside depends on whether additional allocation can be translated into actual commencements without excessive discounting or weakening retention. These universities may have opportunities to compete heavily on prices as expected costs for international students increase from cost-of-living challenges and already expensive visa fees.

Many institutions still rely on enrolment assumptions, fragmented data and intuition rather than an integrated view of enrolments, yield and strategy trade‑offs. These policy changes present a clear opportunity for universities to reset their planning, quantify the revenue implications of policy changes, and deliberately optimise their international portfolio.

Tom Gordon and Ivar Berget work with ConceptSix.